Are Home Improvement Stocks Now Undervalued?

[ad_1]

The lockdowns of 2020 may have prompted buyers to put a lot more funds towards their environment, boosting earnings for residence enhancement vendors Lowe’s (NYSE:Reduced) and House Depot (NYSE:High definition), but the financial and housing availability crunches of 2022 are keeping them there.

Furniture, electronics and house place of work set-ups aimed at producing dwelling a greater area to dwell and operate fueled 2020 purchasing, but with individuals dealing with climbing costs of gas and food stuff, theyre going to dwelling improvement retailers to cope with repairs on their own and start out gardens. This is keeping growth at Lowe’s and Home Depot solid, producing them both of those perhaps lucrative portfolio additions this summer, in my feeling.

Each options have soaring dividend yields, making them attractive for value investors seeking to make passive earnings as properly. Right before you add possibly of these household enhancement shares to your portfolio, however, there are some negatives to think about.

Lowes

Lowes (NYSE:Low) is a residence advancement retail chain working in the U.S., Canada and Mexico. It presents products for construction, servicing, repairs and remodeling. The housing marketplace may well be cooling a tiny from the highs of 2021, which may inspire jobs in the property youre in.

Revenues for the organization have doubled around the previous ten years, and earnings for each share are envisioned to expand all over 13%. Lowe’s has a dividend generate of 1.66%, and the firm has a very long observe history of rising dividends. That could enable sweeten the offer for traders.

Analysts amount Lowe’s a purchase, even while bulls assume the enterprise faces risks from climbing interest charges, source chain troubles and flattening housing selling prices. Its value noting that the median age of households in the U.S. is 39 yrs, an age when houses will need to have an expanding volume of upkeep and could be candidates for reworking.

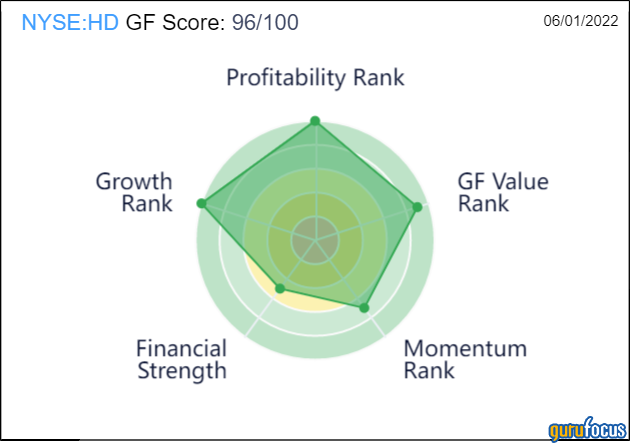

Lowe’s gets a GF Rating of 96, driven generally by prime ratings for profiability and growth.

Dwelling Depot

Surpassing forecasts in nine of the last 10 quarters, an additional important U.S. household advancement retailer, Residence Depot (NYSE:High definition), not too long ago documented 10.7% advancement in web sales 12 months-more than-yr.

Home Depot counts experienced contractors amongst its most important customers, and their massive-ticket purchases were being up 18% during the past calendar year. EPS has grown 17% about the previous a few yrs and income is up 8% more than the earlier calendar year, having it a get ranking from analysts.

Residence Depot has a dividend generate of 2.26%, earning it the much more interesting of these two shares for all those in search of dividends.

Like Lowe’s, Residence Depot also has a GF Rating of of 96/100. In addition to higher expansion and profitability, it scores improved than Lowe’s for GF Price, while it loses details for weaker momentum.

This article 1st appeared on GuruFocus.

[ad_2]

Resource link